Lululemon Athletica (LULU), is a premium sportswear company that has traditionally focused on women’s yoga apparel and equipment. The stock has been absolutely pummeled this year, now down more than 50% from its high in early 2024.

It’s not alone. Retail apparel is currently one of the few sectors left on the stock market’s bargain rack. Low multiples in the space reflect a souring fundamental outlook, with revenue and earnings flatlining or shrinking across most major brands.

When it was touching $160, it was clear that LULU was finally undervalued, but the share price has gained more than 25% in the past month, rising to $210 per share on news of a C-Suite shakeup. We aim to determine whether the company is still a bargain after the 25% gain, what is driving newfound market optimism, and what is realistic to expect in terms of future growth.

We’ll Cover:

The company’s history since the late ‘90s, from massive growth and brand dominance to flagging sales, pivots into new markets and the recent executive shakeup.

LULU’s financial performance, capital efficiency and discounted valuation.

The company’s key leadership, strategic vision over the past few years, and why the current CEO’s departure makes shareholders happy.

Compensation, ownership structure, and Capital Efficiency.

Unique risks and opportunities for the company.

Ultimately, while we do not share the market’s ebullience over new leadership or optimism about the sector’s performance moving forward, we like LULU’s chances of outperforming a portfolio of comparable apparel companies like Nike, Columbia, American Eagle and Under Armour.

History

Origins: Real Yoga Clothes and Early Experiential Retail

Source: Lululemon

Lululemon was founded in 1998 in Vancouver, Canada, by Denis “Chip” Wilson, an entrepreneur with a background in technical apparel. The idea came to him after attending a yoga class in 1997, where he noticed women wearing cotton clothing that was neither comfortable nor functional for yoga. He saw a clear market need: high-performance, flattering apparel designed for real movement.

Wilson’s early setup was innovative. His space was a design studio by day and a yoga studio by night, giving him direct access to practitioners who provided feedback on fit, fabric, and function.

The first standalone Lululemon retail store opened in November 2000 in Vancouver’s Kitsilano neighborhood, a community known for health, wellness, and active lifestyles. Beyond the shop, it was a community hub for yoga and healthy living. It was an early sign of Lululemon’s leadership in experiential retail, which we’ll discuss later.

He named the company Lululemon for perhaps the last reason you would expect: Japanese people would struggle to pronounce the name. At the time (and still today to some extent), Japanese consumers were tastemakers when it came to premium brands. A difficult word which used a lot of the “L” sound (notoriously difficult for Japanese speakers) would give the brand a more authentic “Western” vibe.

The unusual “Lululemon” name soon became a talking point and a kind of grassroots marketing device.

Early Growth and Product Innovation (2001–2007)

From the start, Lululemon focused on innovative fabrics and fit. Its signature material, Luon, blended nylon and Lycra to create a soft, stretchable textile that moved with the body — a huge improvement over baggy cotton.

By the mid-2000s, the brand was expanding rapidly. In 2003, it opened the first U.S. store in Santa Monica, California. In 2004, Lululemon began broader international expansion, including stores in Australia and Japan. Rather than traditional advertising, the company built a community-centric strategy: stores hosted events, employees (called educators) were trained in product knowledge and wellness, and local yoga instructors became brand ambassadors.

This kind of grassroots marketing was ahead of its time, as major brands now copy this approach through pop-ups, festivals, and influencers. In July 2007, Lululemon went public on the Nasdaq, raising $327.6 million for accelerated expansion.

Market Expansion (2008–2019)

With growth came organizational shifts. In 2008, former Starbucks executive Christine Day became CEO and helped scale global operations. In 2013, Founder Chip Wilson stepped down as chairman amid controversy, handing over leadership to Laurent Potdevin.

During this period, Lululemon broadened its product range beyond yoga pants to include:

Running, training, and lifestyle apparel.

A dedicated men’s line in 2014 to tap a growing market.

A luxury streetwear brand, Lab, launched in 2019.

The brand has also leaned into “experiential retail”, where entering the stores offered experiences beyond simply buying products. Starbucks and Apple stores are examples of how this can strengthen brand culture, making stores spaces for community connection and lifestyle engagement.

Diversification, Digital Expansion, and Decline (2020–Present)

In 2018, LULU began to pivot in earnest toward expanding its product offering. It also made serious inroads in China around this time, growing into its second-largest market.

Spurred by the pandemic, 2020 marked a strategic pivot into digital wellness. Tapping into what drove pandemic darling Palantir, the company acquired Mirror, an interactive home fitness platform, for approximately $500 million.

It was rebranded as Lululemon Studio, blending apparel with connected fitness content — a move that deepened customer engagement, diversified revenue, and excited investors. We don’t see the product mentioned a great deal in recent filings, and it’s fair to say that, like Tiger King, the buzz did not make it out of the pandemic.

Lululemon also ventured into footwear, beginning with women’s shoes in 2022 and later expanding men’s offerings. LULU has received mixed reviews on its revenue diversification efforts, which we’ll discuss throughout the report, but non-apparel sales have now grown to 13% of revenue.

By 2024, the company surpassed $10 billion in annual revenue and operated over 760 stores globally. In 2025, that growth is flagging, relying heavily on China and other international markets to sustain 7% growth (and shrinking income) so far this year.

Recent Challenges and Future Direction (2025)

Today, Lululemon faces a competitive and evolving landscape:

Growth in the U.S. has slowed, with sales and share price performance drawing scrutiny.

An activist investor, Elliott Management, acquired a large stake in late 2025 and is pushing for leadership change. The company is suing major retailers (e.g., Costco) over alleged design “dupes,” reflecting tension between premium positioning and low-cost competitors.

These dynamics signal a moment of strategic realignment as Lululemon seeks to reinforce its innovation edge, deepen global markets (including new ones such as India), and evolve its brand relevance.

Unique Business Qualities

Athleisure Leadership

Every premium brand wants to position itself as shaping culture more than selling clothes. In Lululemon’s case, it’s true. The massive shift toward “athleisure”, such as wearing yoga pants to the grocery store or on a coffee date, was arguably started by this company.

High-quality workout wear has become everyday apparel, especially for women. Leggings, once confined to the gym or studio, is a mainstream wardrobe staple today. There is a short list of companies, such as Nike’s running shoes and Levy’s denim, that can claim such a massive impact on everyday fashion.

Lululemon may have been the leader in that shift, but the horses are off to the races. While still the leader in athleisure, especially for women, it is a much more crowded space today. From premium players like Alo to undercutters like Costco, LULU has to fight more than ever before for market share.

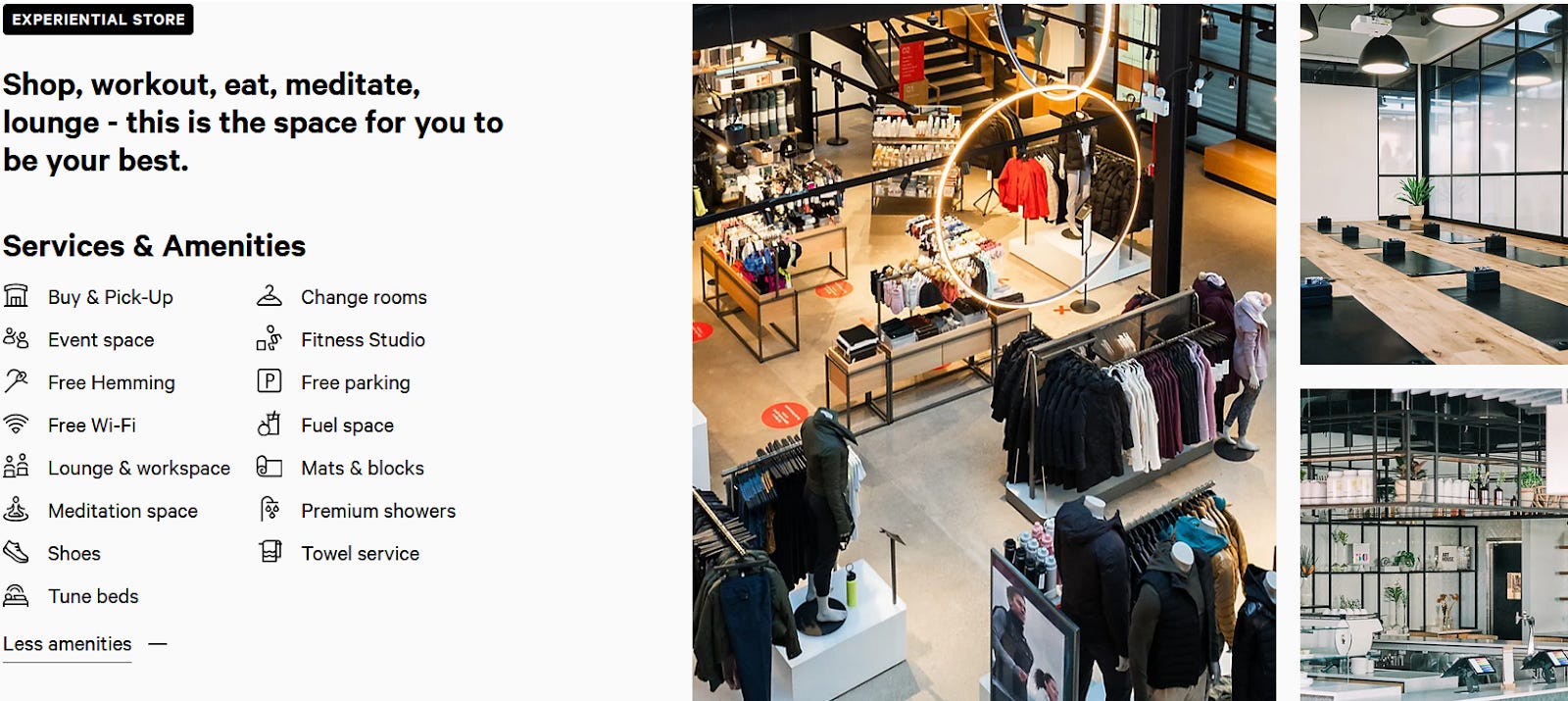

Experiential Retail

Lululemon’s Chicago Location: Keeping you in the Ecosystem

Source: Lululemon Website

Lululemon was one of the first companies to pioneer “experiential retail”. This business model, which really started taking off in the late 2010s, makes the experience of shopping as big a value-add as the product itself.

Many locations offer different levels of experience to accompany your purchase of leggings or a yoga mat. These include meditation and yoga courses, cafes, and coworking areas. This is strong marketing, but as we discuss below, it hasn’t been enough to maintain same-store sales growth.

“Body-Shaming” and Other Controversies

Lululemon has a long and well-documented history of self-inflicted PR problems that mainly stem from public comments by its founder, Chip Wilson. The company’s name traces back to Wilson’s fixation on the Japanese market in the late 1990s; he said that he thought Japanese consumers would struggle to pronounce the letter “L,” and that using multiple L’s would be “funny” or memorable to them.

While this explanation was initially treated as typical “eccentric founder” lore, it has aged poorly and is increasingly read as racially insensitive. Other controversies have compounded, such as his assertion that to preserve the brand, “you don’t want certain people coming in”. The name’s origin reinforced the perception that Lululemon’s early brand identity was less about inclusive marketing and more the founder’s personal biases and limited worldview.

More damaging were the company’s repeated entanglements with body-shaming accusations, particularly during the period when Wilson was still closely linked with the brand. The most infamous episode came in 2013, when Wilson responded to quality complaints about overly sheer yoga pants by suggesting that some women’s bodies “don’t work” for the product.

Much like Hollywood, criticism of these body standards hasn’t been enough to make them go away, and certainly not enough to sink the company.

Aspirational Aesthetic, Exclusive Branding

Chip Wilson won’t win any Nobel Prizes for his comments on Lululemon “not wanting everybody” in his stores, but he also sort of said the quiet part out loud. The brand’s greatest advantage, and what gives it such high pricing power, is its sense of exclusivity and status.

Wilson has stressed that “exclusivity beats inclusivity” when it comes to branding. Although he’s long removed from company leadership, it seems that the legacy of his approach lives on. Charging $100 for leggings and offering a bevy of exclusive “membership” perks helps to both foster a sense of community and a walled garden. Like Apple, those two factors can create significant brand synergy, loyalty, and pricing power.

This approach is particularly effective in the Chinese market today.

Chinese Leadership

LULU certainly isn’t the only apparel brand leaning on the Chinese market to support growth as US demand flags. However, it’s doing it better than other brands.

A Business Insider story also recognized Lululemon’s leadership in the massive market:

“Lululemon entered China with a long-term goal and has invested in a strategic approach to innovation, lifestyle resonance, brand ambassadorship, social media engagement, and global resource integration.”

According to a Reuters interview with a Chinese fitness model Ning Zheng, who markets Lululemon’s products as well as other international sports brands:

“A lot of Chinese women are new to sport, they feel a bit intimidated… But if other people from their yoga studio or running groups, or someone they relate to online, is wearing a brand, they believe it can be good for them too,”

China now contributes more than half of LULU’s revenue growth, which could prove both an asset and liability moving forward. Chinese sales also have higher gross margins than any other market, including the United States.

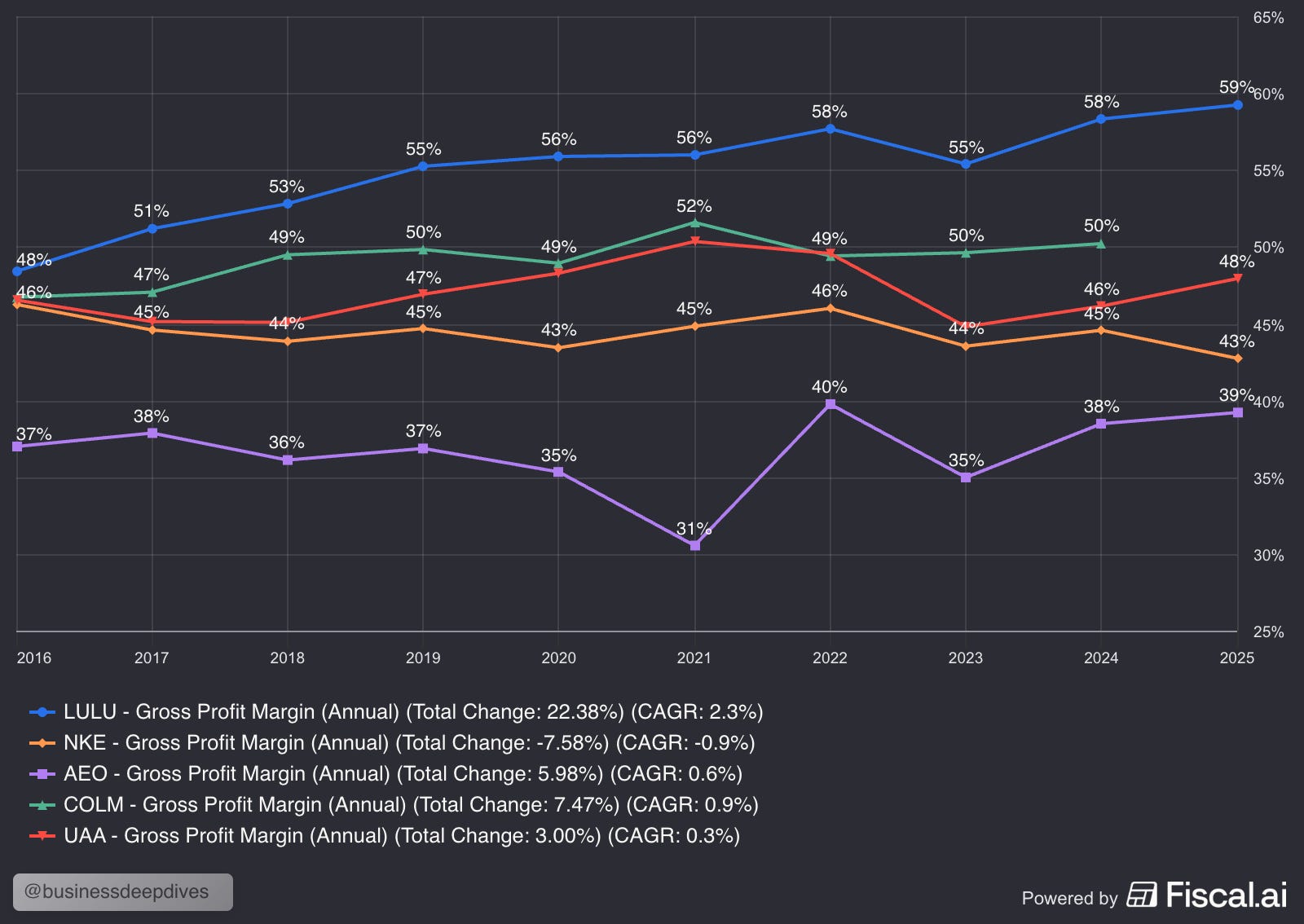

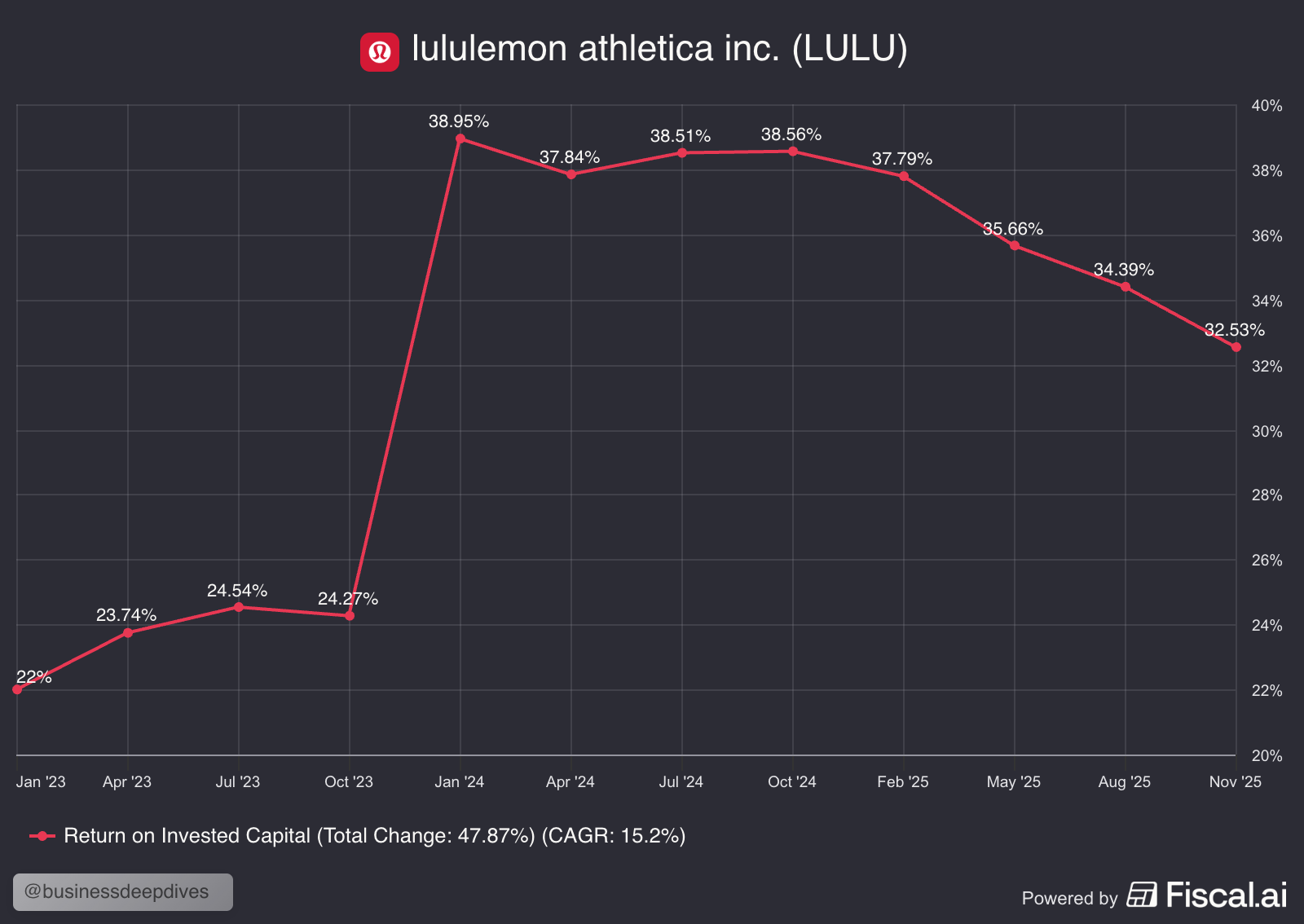

Industry-Leading Margins

Premium branding can be hard to maintain, but boy does it pay dividends. With gross margins in the high 50’s and profit margins north of 15%, LULU is one of the most efficient apparel brands in the world.

Lululemon’s Elite Margins

The chart above shows how LULU is able to leverage a streamlined product offering, anchored in women’s gymwear, and premium pricing to achieve tech-company margins in one of the toughest industries for sustained pricing power.

It is important to note that menswear and its other product categories, such as shoes and yoga accessories, do not carry such elite margins. Women’s apparel, particularly the brand-anchoring yoga pants, are the secret to LULU’s massive margins.

It’s important to note that excess inventory, as LULU is grappling with as it enters the fourth quarter (more on that later), is not a good sign for strong gross margins in Q4.

Business Segments

LULU’s core market, in terms of both brand identity and sales volume, remains anchored in women’s apparel in North America. However, that market is stagnating, and as of recently the company gets all growth from other segments and regions.

The challenge for Lululemon, along with other companies that rely on a premium brand reputation, is expanding its reach while remaining an authority in its original niche.

Product Segments:

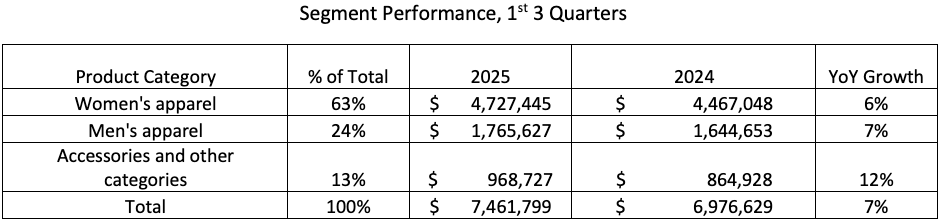

Women’s Apparel (63% of Sales)

Women’s apparel remains the economic and brand core of lululemon. This segment is dominated by leggings, yoga pants, bras, and fitted tops originally designed for yoga but now worn as everyday athleisure.

In North America, the space has matured and is increasingly promotion-sensitive, contributing to lower average order values and margin pressure.

Internationally—especially in China Mainland—the same products retain premium signaling power, which lets Lululemon maintain higher pricing, lower markdowns, and better product margins.

Women’s apparel cushions margins across the company. If it weakens in the Americas, consolidated profitability will likely suffer.

Men’s apparel (24% of Sales)

Men’s apparel has been Lululemon’s most important strategic diversification effort, encompassing training, running, and casual performance wear rather than yoga-centric products.

While the segment has grown steadily and now accounts for a meaningful share of revenue, it lacks the cultural distinctiveness that women’s apparel enjoys and faces heavier competition from incumbent athletic brands. To be frank, a lot of men might feel reluctant to let everyone know their t-shirt is from Lululemon, while women are happier to show the brand off as premium, trendy and feminine.

Margins are structurally lower than women’s core apparel due to higher competitive intensity and weaker pricing power, but men’s products help smooth demand cyclicality and reduce reliance on such a specific segment.

Accessories and footwear (13% of Sales)

This category includes bags, yoga accessories, shoes, and residual lululemon Studio-related products. The category is lower margin than the core offering and functions mostly as a basket-expander. It also leads the three broad segments in terms of growth.

These categories broaden the brand’s lifestyle positioning but are operationally more complex and dilute margins. They have higher logistics costs, less differentiation, and greater price sensitivity.

For this reason, analysts often bemoan the company’s persistent push into the product category of “Other”. It’s one of the biggest reasons that the market was happy to see the current CEO Charles McDonald go, as there is a strong sense that this push has not only harmed margins but LULU’s brand as well. We’ll tackle that narrative in greater detail in the Brand Risks section.

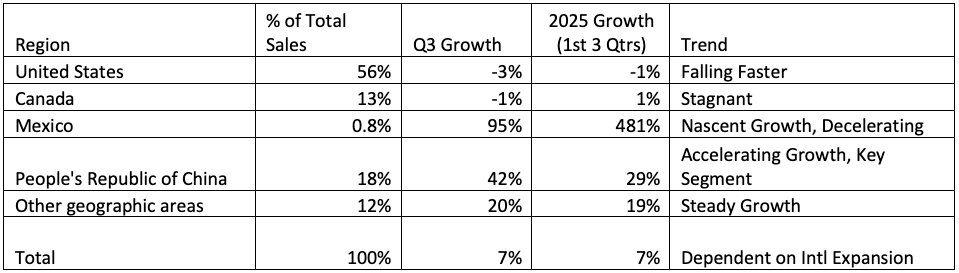

Regions

In its filings, LULU breaks down its revenue by every country in North America (US, Canada and Mexico) and China. The other broad category is “International”.

US and Canada: (68% of Sales)

North America remains lululemon’s largest and most established market. Historically, this region has accounted for roughly two-thirds to three-quarters of total sales, with the U.S. alone bringing in more than half of company revenue, and Canada contributing a stable mid-teens percentage.

One of the most concerning trends for the company is that growth is seriously flagging in both the US and Canada, particularly the United States. Sales growth, and importantly comparable (same-store) sales, are both in negative territory this year for the region. As CEO Calvin McDonald noted in a recent earnings call:

“Americas revenue decreased 2% on both a reported and constant currency basis, with comparable sales down 5%. By country, revenue decreased 3% in the U.S. and was up 1% on a reported basis and flat on a constant currency basis in Canada.”

The North American consumer base still defines lululemon’s scale and core cultural positioning — especially in women’s apparel — but the region is no longer a growth engine for the company. As competition intensifies and discretionary spending patterns shift, this is going to be tough to reverse.

International markets, especially China and recently Mexico, are picking up the slack to keep growth positive.

China (18% of sales)

Regionally, China acts as a premium amplification market for lululemon’s product mix, particularly women’s apparel, where fitness, yoga, and wellness have increasing aspirational value. As Chip Wilson envisioned for the Japanese market, the premium Western aesthetic and focus on wellness and performance has fostered a loyal client base in China.

Higher full-price sell-through, rapid store expansion, and strong e-commerce engagement allow the company to extract higher operating margins than elsewhere, despite some pressure on average order value.

In contrast, the Americas function as a volume-heavy, margin-compressing base, where the same products face saturation, discounting, and declining traffic, forcing lululemon to rely on international markets to sustain overall growth.

Importantly, the 10Q shows that gross margins are higher for China than the US core market. Our interpretation is that discounts are less necessary thanks to China’s robust demand, and the sales mix leans more heavily toward the high-margin core offering (women’s fitness apparel) rather than accessories or men’s apparel.

Mexico (~1% of sales)

Mexico is a small but strategically emerging part of LULU’s global footprint, and sales are on track to grow by roughly 100% this year.

It was added as part of the company’s expansion of the Americas segment after lululemon acquired local operations in late 2024, and while it currently contributes a modest share of total revenue, it represents lululemon’s first foothold outside its traditional North American base in a large, culturally adjacent market.

Mexico’s role today is principally incremental, helping deepen lululemon’s presence in Latin America. That’s a market with a growing consumer base and increasing interest in the type of fitness apparel and aspirational style that the company sells.

Rest of the World (12% of sales)

“Everywhere else” comprises lululemon’s operations outside the Americas and China Mainland, primarily Europe, the Middle East, and Asia Pacific (excluding China).

Although this combined segment still makes up a smaller slice of total revenue it has been growing at rates well above North America and gets more strategically important at the core market matures.

Europe and the Middle East account for a network of stores and digital channels in markets such as the U.K., Germany, and France, while APAC covers markets including South Korea, Japan, Australia, and Southeast Asia.

Channels: In-Store Sags, Online Soars

LULU’s primary two channels, like most retailers, is through online and brick-and-mortar stores.

Q3 Sales Mix

While the company stills sells more product in-person than online, a brand famous for experiential retail is grappling with shrinking in-store revenue. Online sales , which led revenue higher with 13% YoY growth, are making up for a 3% fall in store sales.

This situation is hardly unique to LULU, but it bears close observation as the company continues to expand its retail locations.

Fundamental Analysis

For a company with one of the lowest PE ratios in the stock market today, LULU’s financials could certainly look worse. It has a very safe balance sheet, and is able to afford consistent dividend share buybacks to reward investors.

Growth is where lululemon increasingly falls short. As discussed, the company’s growth profile is flattening in its core market, although international markets (especially China) have kept total growth around 7% so far this year.

Balance Sheet

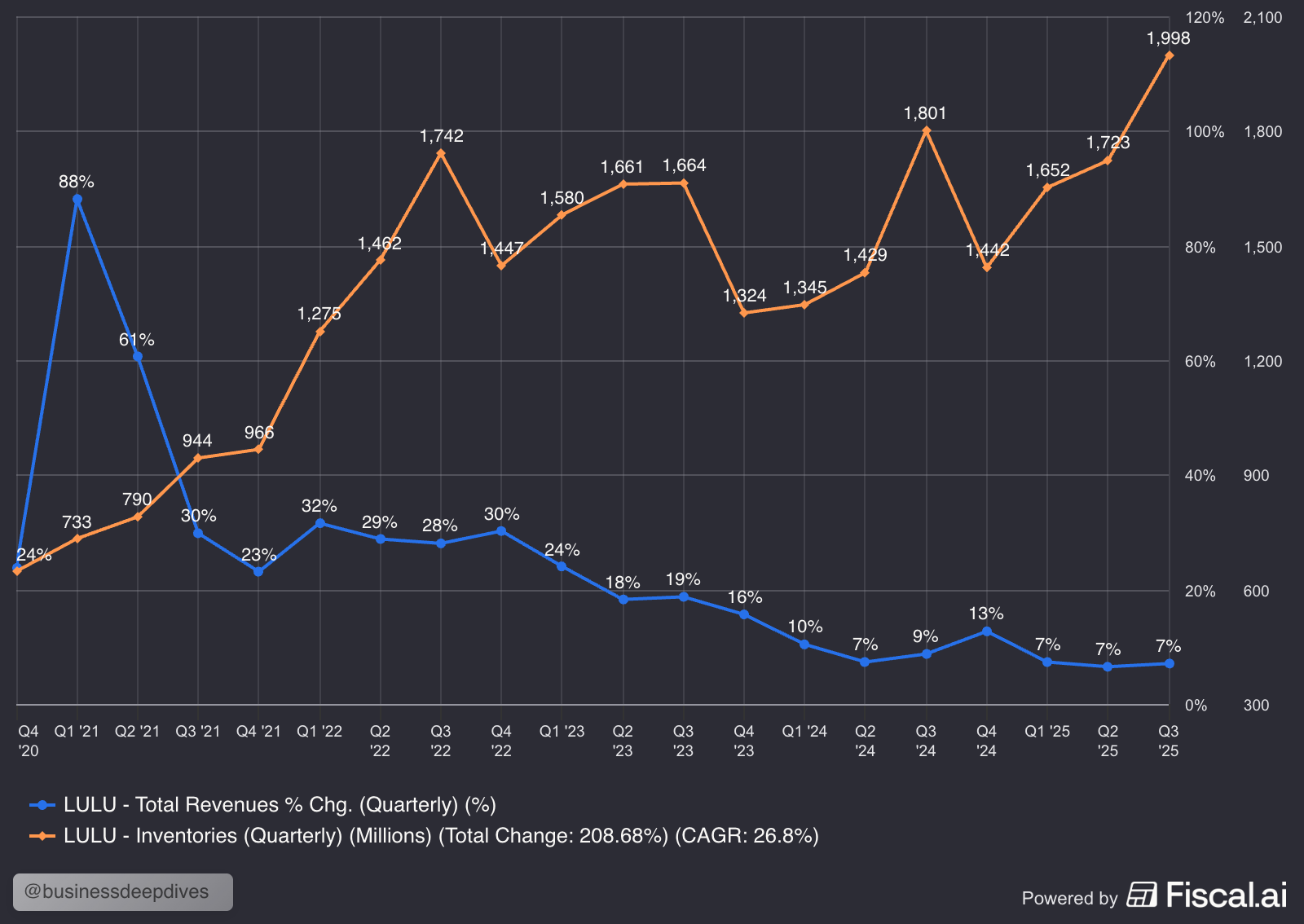

Inventories: Promos Ahead

Inventories have been steadily rising in excess of sales over the past couple years. This was accelerated in early 2025 when Lulu, like many companies, put the gas on order before tariffs harmed supply chains.

Inventory is ramping up while sales growth is slowing down.

Inventory turnover for the past twelve months is 6.4, which isn’t terrible but is not where the company wants to be. As the CEO confirms, a combination of underwhelming sales growth and stocking up ahead of tariffs has put the firm on the back foot.

Q4 could look rough for LULU from a growth and profitability standpoint. They will likely have to lean on promotions to drive sales and wind down inventory to clear space for new products. We discuss inventory issues more in the Risks section.

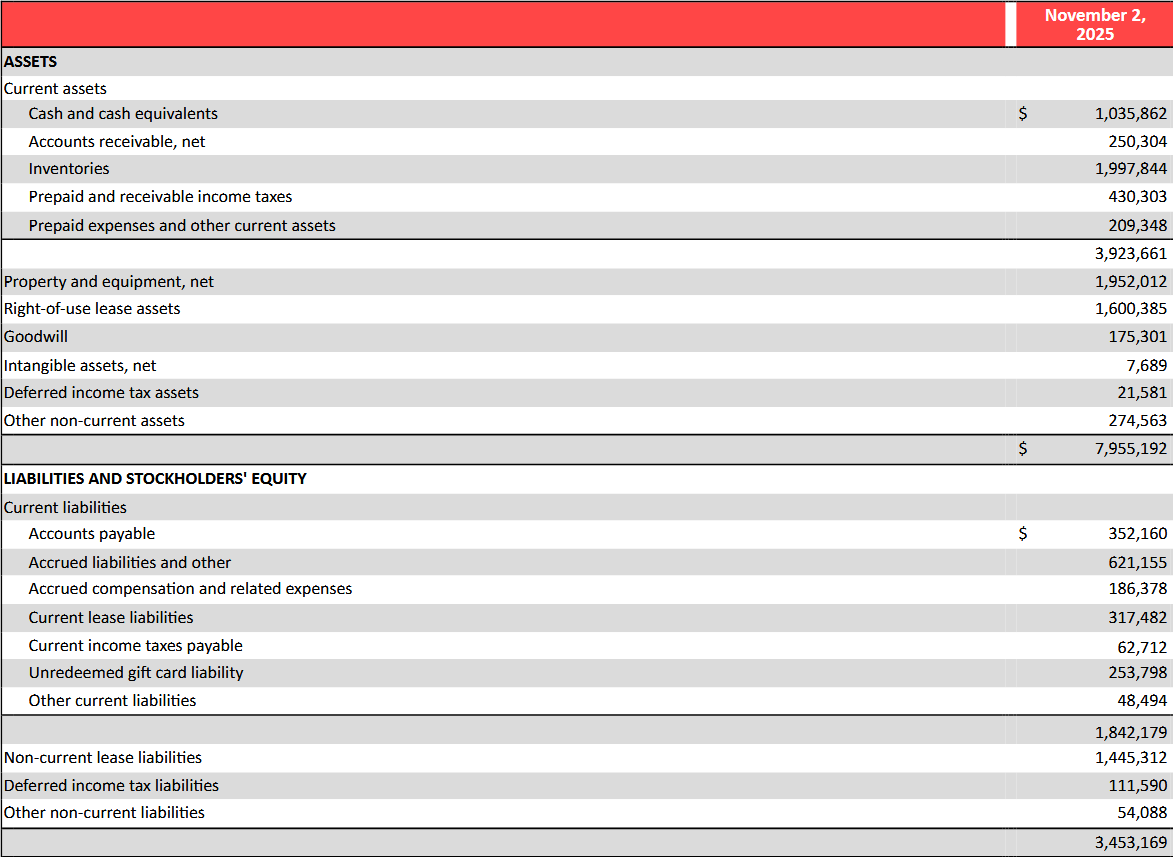

Debt: (Almost) Nothing to See Here

Aside from being a bad name, there’s a reason the company isn’t called LuluLeverage. Take a look at the table below:

LULU: Virtually no Financial Debt

The snapshot from the company’s most recent balance sheet shows a conservative company that leans heavily on growth from earned capital, rather than external financing. Against nearly $8 billion in assets, LULU has just $3.5 billion in liabilities.

Of that $3.5 billion, nearly $2 billion is related to (mostly long-term) lease liabilities.

Per LULU’s most recent 10Q:

“Our leases generally have initial terms of between two and 15 years, and generally can be extended in increments between two and five years, if at all.”

These leases do present some unique risks to Lulu, as they will likely incur some expense if they decide to close a store and exit the lease early, including paying full rent for the remainder of the lease if they can’t find a buyer.

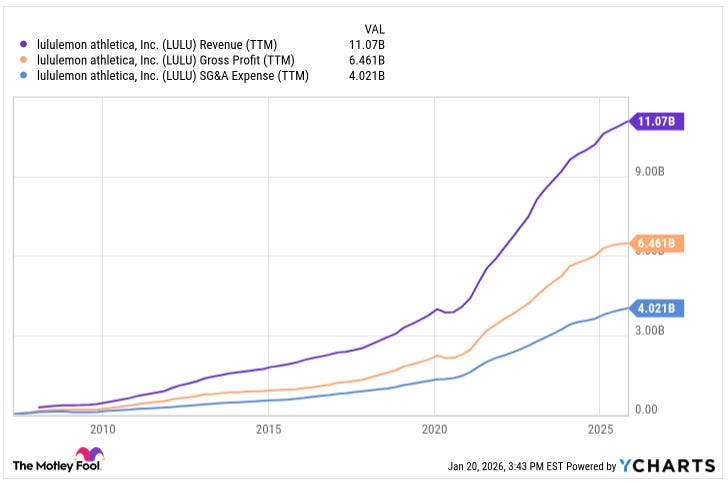

Income Statement

You won’t find anything in the income statement to terrify or inspire you. The story we see in the financials is the same narrative that has dampened LULU’s stock performance: the company is stagnating but it’s far from free-fall. For a different company, flattening growth might look like natural maturity, but when retail brands start to stagnate, it can be a bigger red flag as the effect tends to snowball.

Flagging Growth

A company doesn’t lose half its share price in a bull market for nothing. LULU’s struggles are first and foremost at the topline. Its revenue growth is on pace for 7% (I suspect it may be lower after Q4), driven primarily by the Chinese market.

As we discuss throughout the report, and what scares analysts the most about LULU, is the shrinking sales in the US, historically its most important market. That trend appears to be strengthening.

On the other hand, international expansion is trying to make up for it. Overseas growth and especially China alone saved lululemon from revenue contraction this year.

As we discuss in the Risks section, the company is increasingly reliant on China as both a driver of growth and has always been reliant on the country as a central node in the production chain. The US and China have, to understate, a complicated relationship, and this level of concentrated risk might be a bigger red flag than any other factor for the company.

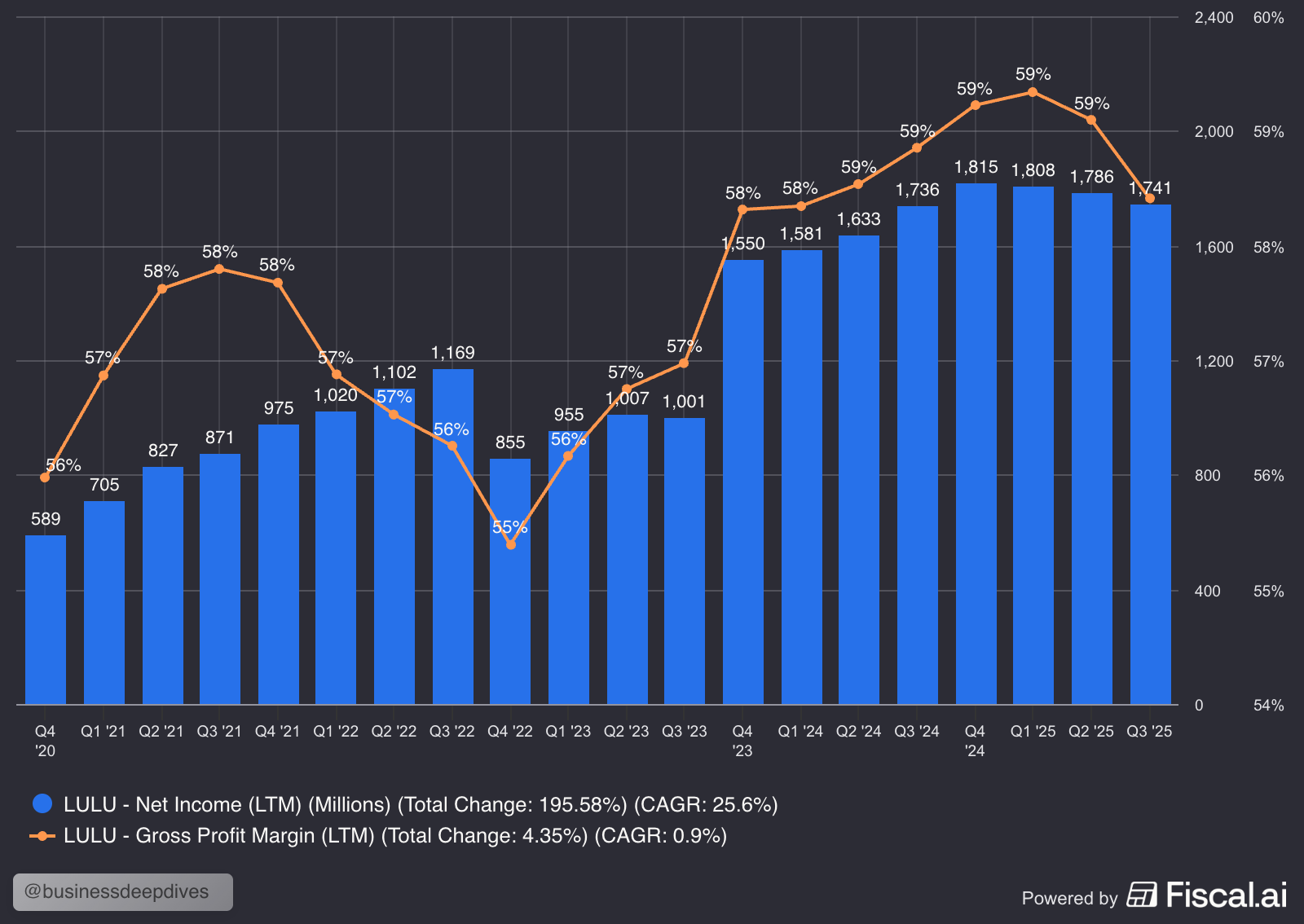

Net income is on pace to shrink slightly this year. However, it could certainly be worse in the case of LULU. While growth is flagging in the US market, it has generally maintained strong margins even here.

The company has no interest expense to speak of, thanks to zero debt. Its long-term lease obligations are potentially a lodestone, as we’ll discuss in the Risks section, but it keeps the company agile and, on paper, extremely efficient with its capital.

It also is achieving some growth in a very tough market for apparel brands.

How LULU Stacks Up

Outperforming on margins and multiples

Despite flagging growth, Lululemon’s profit margins are still impressive, especially for a company in retail apparel. LULU’s premium positioning and pricing power give it hefty gross margins, which feed into an elite total profit margin of over 15%. That blows relevant competitors like Columbia, American Eagle, and Nike out of the water.

Part of the reason for outperformance is LULU’s high apparent return on physical locations.

Low Rent, Long-Term Obligations

As we discussed in the balance sheet section, LULU has no significant financial debt, but it does have some fairly large lease obligations. Looking at the current portion of Q3’s lease obligations, we can estimate that LULU spends about $317 million per year on rent.

Lulemon Stores: Comfortably in the Black

While some of that relates to distribution and manufacturing, we can conservatively estimate $315 million as total store rent to roughly gauge how stores are doing from a profitability standpoint. Total store sales (See Channels in the Business Segments section) are about 60% of revenue. Assuming an even mix between online and in-store, that means that roughly $4 billion of LULU’s gross profit over the past twelve months was earned in stores.

In 2025, in-store sales are enough to cover the entire SG&A budget, which of course includes in-store staffing, even when we overestimate the rent expense. That’s a much rosier situation than those companies who are dying a slow death on shrinking foot-traffic at costly physical spaces.

However, rent obligations may present a challenge as lululemon’s core sales mix shifts online and away from a more expensive brick-and-mortar model. We discuss that further in the Risks section.

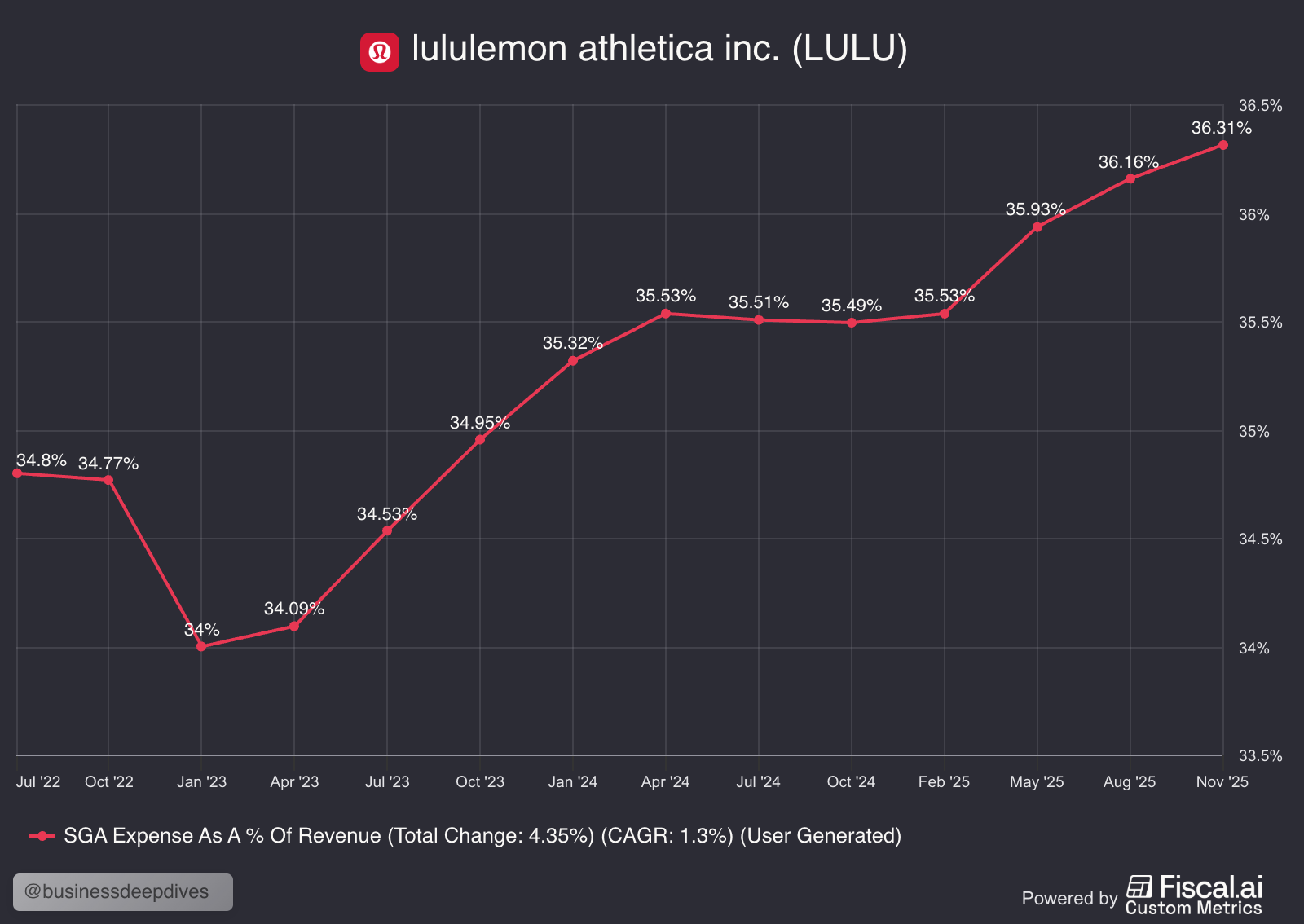

One figure that we’re watching is rising SG&A as a percentage of revenue. We see two primary explanations for this trend:

The company is relying on store expansion (14 new stores last quarter) to drive growth, especially in the American market. Comparable store sales were down 5% in the US, while 11 new locations were opened there. Higher SG&A per dollar sold reflects worsening unit economics, including revenue per store. .

As LULU’s sales mix leans toward more complicated segments (accessories, shoes, etc), it has to take on higher fixed operational costs. To oversimplify, managing a product line that is mostly leggings is a lot less complicated than managing handbags, shoes, yoga mats, and menswear, especially if you want to maintain the same level of quality.

We’ll keep an eye on SG&A in the coming quarters, and while we don’t like the trend, it remains at a manageable level.

Cashflow and Valuation

LULU’s free cash flow has taken a hit over the past year, but the company still looks undervalued:

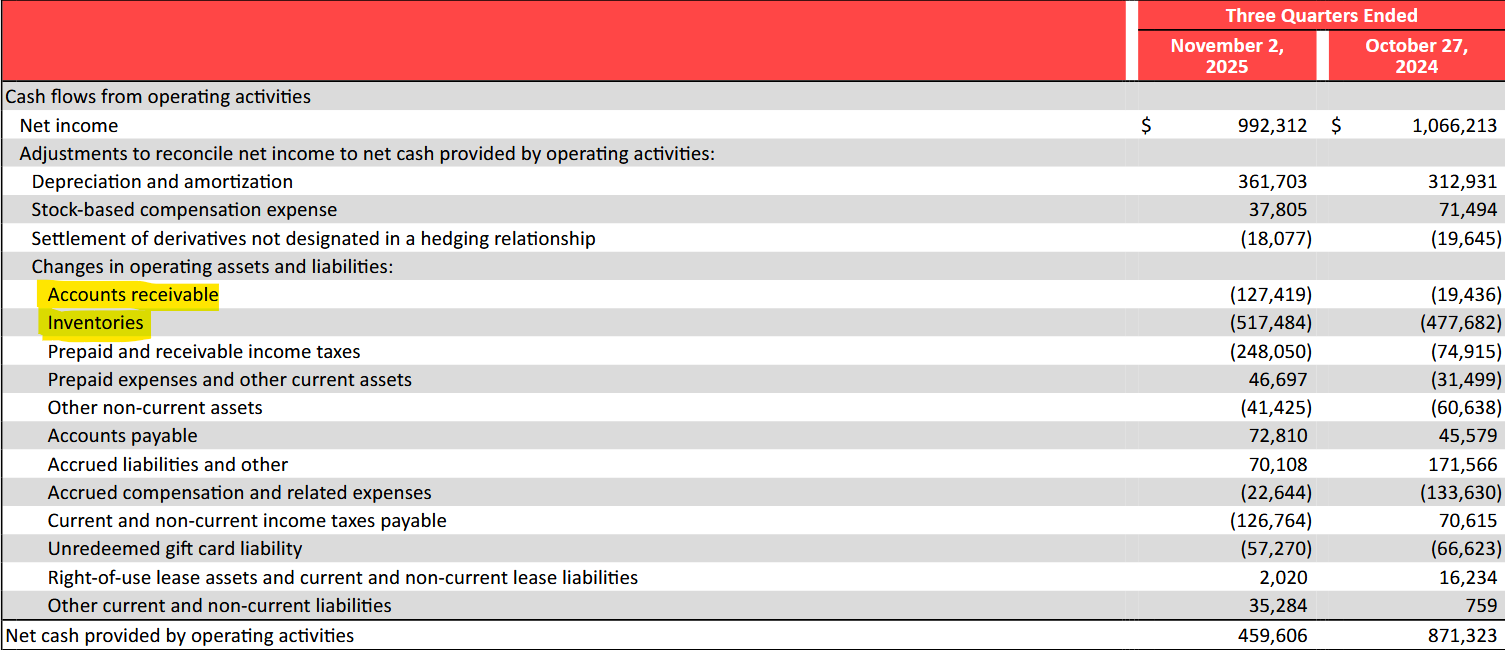

LULU: Losing Cash to inventory and receivable timing

As the chart above shows, the recent dip in free cash flows is mainly due to two factors: lower receivables turnover and excess inventory. We discuss excess inventory, driven by tariffs and lower-than-expected sales, in the Risks section. We expect Lulu to adjust its inventory management moving forward.

Growth in receivables and inventories contributed more than 50% of the roughly $400 million drop in operating cashflow from Q3 of 2024. The other roughly $200 million is due to prepaid income taxes, and is more of a timing issue. We aren’t particularly worried about the dip in cashflow, nor that average receivable collection times have increased from roughly four to five days since 2024.

DCF Valuation

At a share price of $210, the Stock is now fairly valued under the following assumptions:

A discount rate of 10%

9% average earnings growth over a 10-year period.

4% terminal growth thereafter.

We can quibble about whether LULU can maintain 9% growth, which will likely depend on the pace and sustainability of international expansion. The Chinese market is growing fast and provides better margins. That will boost LULU’s topline figures as it comprises more of its sales, and as long as that trend holds, 10% growth is achievable even if North American revenue stays flat.

Regardless, LULU has by far one of the cheapest valuations in the market in terms of multiples, especially within this sector (see Risks and Opportunities section). In contrast to the broader stock market, and the retail apparel sector which is fundamentally underperforming LULU on average, LULU’s valuation today is sane and even cheap.

A correction is likely to hurt LULU less than the S&P or retail sector, which makes it attractive in a relative sense.

Capital Efficiency

WACC Vs. ROIC

We see that Lululemon has a strong value-add when comparing WACC (Weighted Average Cost of Capital) to ROIC (Return on Invested Capital).

There’s a wide and persistent spread between ROIC and its cost of capital. Its WACC is essentially the cost of equity, since LULU has virtually no debt. We can defensibly call it 11%. With the company’s hurdle rate basically equal to equity risk, ROIC seems to comfortably make up for it.

LULU: Highly Capital-Efficient

Against this benchmark, LULU’s ROIC looks fantastic. It historically has been conservative about deploying capital and its hefty margins generate strong returns on what it does invest.

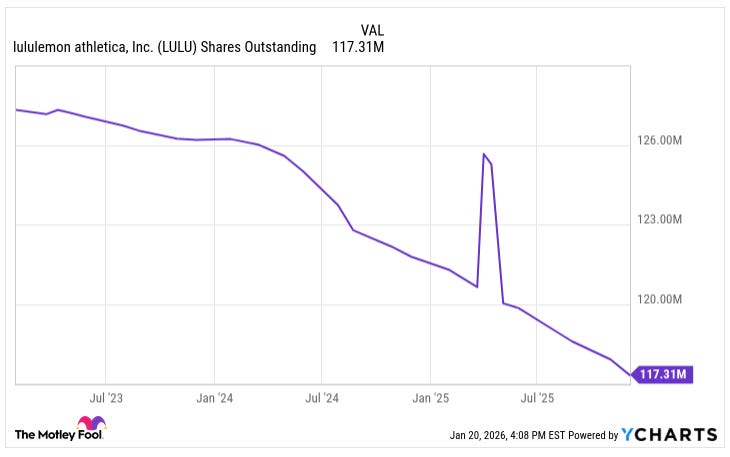

Furthermore, the company has been dutiful about share buybacks.

Buybacks, Dividends

LULU: Giving Back through Buybacks

Lululemon’s capital return strategy has prioritized share repurchases rather than dividends. This makes sense for a company that is so productive with its capital and has historically been in a high-growth stage. Share buybacks, which it provides aggressively and often, have served as a release valve for surplus cash generated beyond reinvestment needs.

Shares outstanding are down 10% over the past five years, with the company retiring about 4% of outstanding shares per year through buybacks. That’s more than enough to offset dilution from stock-based compensation.

Stock-Based Compensation

Stock-based compensation has been modest but not trivial. Based on the most recent disclosures, SBC runs at roughly ~3–4% of net revenue, placing it above pure cash-pay retailers but well below software or platform peers. In absolute terms, SBC is meaningful enough to warrant attention, but it does not dominate the cost structure nor materially distort operating margins.

From a shareholder’s perspective, it’s nice to see dilution from SBC not only neutralized but reversed by aggressive share buybacks.

Leadership and Ownership Structure

Ownership Structure

Lululemon has a single class of common stock, with no dual-class or super-voting share structure. This simplifies governance relative to many founder-led consumer brands, and allowed the company to part ways with the controversial founder Chip Wilson. Ultimate control lies squarely with common equity holders.

Insider ownership is not controlling. Founder Chip Wilson remains the largest individual shareholder with about 8% of the company. Insider ownership is quite trivial, and institutional investors own about three quarters of the float.

Key Leadership

Calvin McDonald: Outgoing CEO

McDonald has served as Lululemon’s CEO since 2018 and is widely credited with engineering the company’s transition from a founder-driven, occasionally erratic brand into a more disciplined global retailer.

Under his leadership, Lululemon delivered consistent revenue growth, expanded meaningfully outside North America, and broadened its product portfolio beyond women’s yoga apparel into men’s, footwear, and accessories. The last part is why many investors are happy to see him go, as they feel this diluted the core brand and stretched operations into more lower-margin, logistically complicated segments.

McDonald played a central role in distancing the company from Chip Wilson’s public persona, emphasizing inclusivity, community, and performance rather than ideology. His tenure coincided with improved execution in supply chain, digital, and omnichannel retail, helping Lululemon sustain premium margins at scale. He may prove to be a bit of a scapegoat for the more structural slowdown that LULU has experienced over the past couple years.

Meghan Frank, CFO, Interim Co-CEO

LULU’s CFO for years, Meghan Frank will maintain heavy continuity as she steps into the interim co-CEO role. As CFO, she has overseen capital allocation, margin management, and investor communications during a period of rapid growth and heightened market scrutiny. Importantly, there was clear consensus between McDonald and Frank, meaning that she likely agreed and contributed to most of their strategic decisions.

Frank is closely associated with Lululemon’s disciplined approach to store expansion, inventory control, and return on invested capital, making her a steadying presence during the leadership transition.

André Maestrini: President & Chief Commercial Officer, Interim Co-CEO

Maestrini represents the commercial and execution-oriented side of the interim co-CEO pairing. After joining lululemon in 2021 to run International, he was elevated to President and Chief Commercial Officer in 2025—an unmistakable signal that the board wants tighter global coordination across regions, channels, and go-to-market decisions.

Maestrini gets major credit for turning international from “nice optionality” into a real growth engine, scaling the model across EMEA, APAC, and China while institutionalizing the operational discipline that’s required when a brand moves from cult-status to global incumbent. Skeptics will argue that international momentum is partly “easy growth off a smaller base,” and that it doesn’t automatically solve North America’s maturation issues. Fair—but that critique misses what this promotion actually telegraphs: the board is prioritizing integrated commercial leadership and consistent execution over a wholesale strategic reset.

His elevation also suggests the company is not, at least yet, in “rip it up and start over” mode. Pairing a global operator with deep brand-building experience (including a long run at adidas) alongside the finance function is a very particular kind of answer to the moment: simplify, integrate, and re-sharpen execution—then let the results speak.

Continuity First

This may seem cynical, but we see LULU’s leadership “shakeup”, and the nice long 6-month transition period to a new permanent CEO, as a way to appease the market without making serious change. In our opinion, the board might as well be saying this:

“We know the market blames McDonald for flagging growth, but we think he did pretty well. We’ll fire McDonald to boost sentiment (which worked), but the interim co-CEO’s have been just as instrumental to Lulu’s operations and brand strategy as McDonald himself.”

To confirm this narrative, McDonald isn’t exactly jumping ship. He’ll continue as a major strategic advisor at least through March of 2026.

Risks and Opportunities

The biggest risk to LULU’s share performance is gradual shrinkage in its core segments (North America and women’s apparel). Most risks sort of orbit around that key niche, but since the company has virtually no debt, any decline will be slow, with plenty of time to see the writing on the wall, rather than a massive drop in earnings, revenue, or solvency.

Brand Risks: Over-Extension, Under-Expansion, and Natural Decline

Natural Brand Risk: Father Time is (Almost) Undefeated

Lululemon has long been the brand in premium athleisure, especially when it comes to Yoga. It practically invented the category, blending technical performance with aspirational lifestyle appeal.

However, the landscape is shifting, and changing brand preference presents a significant strategic risk. In recent years, competitors such as Alo Yoga, Athleta, and even high-fashion entrants have eroded Lululemon’s category dominance. Along with premium competitors, functional, stylish athletic apparel is available at much lower price points.

Consumers—especially younger, trend-sensitive segments—are increasingly drawn to brands that emphasize fashion-forward design, social media visibility, and inclusivity, rather than just the technical quality or established presence that Lululemon is known for. The company risks losing the “halo effect” that has historically allowed it to ask over $100 for a pair of leggings.

This issue definitely is not unique to Lululemon; apparel brands often see cycles of ascendancy and decline as consumer tastes evolve, and some even make a comeback. There are very few apparel brands, like Nike or Levy’s, that manage to stay relevant for decades. Lululemon has yet to prove that it has that kind of juice.

Brand Over-Extension

Beyond the risk of Lululemon’s brand naturally falling out of favor, strategic mistakes could compound the problem as well. Many analysts are happy to see new leadership because of Lululemon’s expansion since 2018 into new product categories and lifestyle segments, such as footwear, personal care, and home wellness. While these moves diversify and broaden its ecosystem, they carry the inherent danger of diluting the brand’s core identity and have definitely hurt gross margins.

As Jeffries senior analyst Randy Konik recently explained on CNBC:

“So what we noticed a couple of years ago is the management team was trying to stretch, pun intended, in the wrong directions with the company. They were running out of gas in the core with the leggings product, and they were starting to try to sell non-core products to non-core customers. Teenyboppers with the belt, bags, sweaters, logo products, ankle length skirts… It just didn’t work. And with that leadership strategy, they kept at it… It’s been a number of years. It just didn’t work. The US business is fading. So with the leadership departure today or announced last night, that’s a big positive for the business.”

Randy (and LULU’s financial statements) make a pretty compelling case that the strategy hasn’t been able to save growth in the US. However, sometimes “let’s get back to what works” can ring hollow when the women’s athleisure market is finite, increasingly competitive, and not as trendy as it was in the 2010s.

Additionally, the argument once again builds from the premise that McDonald stepping down is a major leadership shakeup, which it is not, at least for now.

Brand Over-Concentration

I personally find the “they’re doing too much” argument to be less compelling than market-watchers, which is why the leadership change is less of a bullish signal. Actually, I doubt the strategy will meaningfully change under new leadership and I doubt that it would help to change it. There is an assumed causality between flagging growth in Lululemon’s core offering and the emergence of menswear and accessories as major segments.

Men’s apparel and other “non-core products” have been outgrowing LULU’s core apparel offering for years now, albeit from a smaller base. Furthermore, we can assume that a massive share of the growth in women’s apparel is driven by the Chinese market, judging by superior margins in Chinese sales.

I understand the challenge of expanding the net without stretching brand identity, especially for a premium brand. What is hard to accept is the counterfactual, that if LULU hadn’t pursued non-core segments, its women’s athleisure sales growth would have been so much larger that total revenue and profits would be higher today.

I think Lulu’s struggles are more structural than strategic, and that’s a tougher pill for the market to swallow. It certainly takes more than reshuffling existing leadership to restore confidence if that’s the case.

Overall, shifting brand preferences underscore the fragile nature of brand dominance in apparel. Lululemon faces the dual challenge of defending its identity and technical credibility while also remaining culturally and aesthetically relevant in a fast-moving market. Without careful management of these tensions, the company risks losing its unique positioning, eroding pricing power, and ceding ground to disruptors.

This pattern—of once-dominant brands losing relevance amid evolving tastes and competitive pressures—is a recurring theme in the apparel industry. It’s a minefield, especially if you’re under intense pressure to maintain steady growth every quarter. That’s why LULU is leaning so hard overseas, especially the Chinese market. Speaking of which…

Overseas Dependence, China Concentration

We’d Like to Thank China…

LULU, perhaps involuntarily, is staking its growth outlook on continued international expansion.

On a recent earnings call, McDonald laid out LULU’s strategy to outrun troubles in its core market:

“We have broadened our global reach from 18 to over 30 geographies and grown the company’s China Mainland business into our second-largest market. We expanded the horizon for what’s possible for Lululemon: quadrupling our international business, growing our men’s business, as well as our online channel, and extending into new categories and activities.”

China is now the number one driver of sales growth, by far, for LULU. To provide a startling figure, China has provided over 60% of Lululemon’s sales growth so far in 2025. The figure is even higher for growth in gross profit. That is some major dependence on the Chinese market for an American company.

All it takes is a diplomatic dispute, or a comment about Taiwan by LULU’s erratic founder, or an actual conflict between the US and China, and the company’s growth virtually disappears. Lululemon is leaning more and more on China to save flagging growth, which is logical, but it’s a very fragile base to build upon.

Beyond selling to China, Lulu also sources significantly from the country, as well as some other states that present supply chain risks.

Supply Chain Vulnerabilities

Like most apparel brands, Lululemon’s sourcing chain is fairly concentrated across a few key countries, virtually all of them in Asia. China is not only LULU’s main growth driver, but it is an essential part of its supply chain as well.

To quote last year’s 10K:

“During 2024, 40% of our products were manufactured in Vietnam, 17% in Cambodia, 11% in Sri Lanka, 11% in Indonesia, and 7% in Bangladesh…

During 2024, 35% of our fabrics originated from Taiwan, 28% from China Mainland, and 11% from South Korea, and the remainder from other regions.

We also source other raw materials… from suppliers located predominantly in APAC and China Mainland.”

The issue is the same for most international businesses: geopolitics tends to butt into Sino-American trade. Selling to and sourcing from China, especially to an increasing extent, puts Lululemon in a vulnerable position.

It’s certainly not the only apparel company with this vulnerability, but we must remember that 60% of sales growth and 28% of its fabrics are now provided by the country. If that’s not a risk, then we need to revisit the definition.

Unproductive Leases, Over-Expansion

LULU is adopting a popular tactic for retail brands with flagging growth: more stores! The company opened 12 new locations last quarter, 11 of them in the US, and has signaled an intention to keep the train rolling.

At the same time, stores are producing less revenue. Same-store sales were down 5% in the United States (yikes), while all in-person retail shrunk about 3%.

As discussed in the Fundamental Analysis, the company’s estimated gross profit from physical stores is strong enough to cover rent (which is currently about $315 million per year) and all other general/administrative expenses. That’s pretty good, considering that online retail now constitutes roughly 40% of revenue.

The issue is that LULU, to maintain a lean capital base and stay agile, signs very long leases, sometimes up to fifteen years. According to its filings, it usually doesn’t have any option to jump off the boat early.

As the company keeps expanding stores, and revenue per store falls, we’re going to see margins continue to shrink in the near term. In the longer-term, we may see LULU have to either subsidize the rent on less productive stores or abandon stores that they’re still on the hook to pay the lease for.

Since total lease expense comprises less than 20% of annual income, this is not an existential risk. However, when you try to outrun shrinking same-store sales by expanding locations (a very old trick in retail), it tends to lead to slimmer margins and headaches down the road.

Excess Inventory, Tougher Margins

Like other retailers, LULU frontloaded its orders in anticipation of tariffs in early 2025, and the year’s sales haven’t been enough to make up for it. Hot take: LULU’s margins and sales growth are going to be worse next quarter than in Q4 2024. The smoking gun is over-inventory.

This is actually not a hot take at all. Even CEO Calvin McDonald alluded to the issue in the most recent earnings call:

“So this year, as you know, sales haven’t met our expectations, and therefore we have more seasonal inventory that we’re clearing through, and that’s reflected in our markdown expectations. As we started planning next year, we are taking a more conservative posture on inventory.”

As we discussed, inventories are up and turnover is falling. To trim the inventory figure and clear up rack space for new lines, the company is going to have to run some discounts. Even then, sales volume may not be enough to bring inventory turnover above Q4 of 2024.

To confirm a tougher margin outlook for Q4, take a quick browse through Lululemon’s discount page, aptly named “We Made Too Much”. An even more honest name would be “we should have taken a more conservative posture on inventory to reflect slowing sales growth”, but that doesn’t have the same ring to it.

Next quarter, LULU will likely see gross margins shrink as it offloads excess inventory, and while it will be the year’s biggest quarter saleswise, YoY revenue growth is unlikely to crack 10%.

A Bet on Beating the Sector

In a vacuum, Lululemon is one of the least enticing companies that we’ve covered so far; it doesn’t have a credible moat, strong growth, or industrywide tailwinds. Apparel is a famously fickle business, with trends and brands falling out of favor at the drop of a hat. On top of that, the macroeconomic and geopolitical climates suggest rough weather ahead.

Changing consumer tastes, price sensitivity, geopolitics and tariffs are all weighing on LULU, just like they’re weighing on virtually every other apparel brand. What’s great about a highly financialized market is that you can still profit from LULU’s relative undervaluation; future headwinds are much more priced in than for comparable companies.

The reason LULU warrants a close look is that it is very well-positioned within a poorly positioned sector.

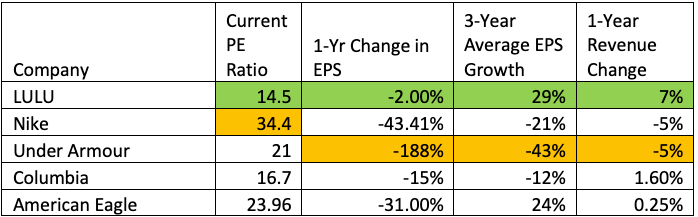

This chart tells me two things: the retail clothing sector is the sick man of the stock market. Across the board, we see flagging revenue and earnings across spaces. Premium athletic brands like Under Armour, Columbia, and Lululemon have all suffered, particularly in the American market.

There are major structural factors, such as consumer price sensitivity hurting volume and margins, increased competition from other athleisure and premium fitness brands ,and tariffs eating even further into bottom lines. Of course, geopolitical pressure casts uncertainty on both supply chains and the predictability of the Chinese market, which famously will boycott or ban brands that offend its sense of nationalism.

However, you likely see something else among all those companies: Lululemon appears to be faring the least badly, and yet it has the lowest PE ratio of all. In case it didn’t immediately jump out, I highlighted the most and least attractive companies in terms of earnings/revenue growth and PE ratio.

Lululemon may not be the Wall Street darling that it once was, but the lumps that market has doled out have brought it to an attractive place from a value perspective. Its days of double-digit growth and American athleisure monopoly may be behind it, but it is still growing and seems to be plowing through a tough environment more quickly than competitors.

How to Capitalize?

Even after recently climbing 25%, the company’s share price relative to performance still doesn’t make much sense, when compared to the broader stock market and certainly when compared to a sector that is generally hurting much more.

It’s important to note that we’re more interested in the relative undervaluation than the bullish thesis. We’re skeptical that leadership, which for the foreseeable future will be quite similar to the current team, will somehow propel LULU against the very obvious market headwinds that are driving just about every comparable company backward as well.

What we like about LULU is its demonstrated endurance over the past couple years to plough against those winds better than competing companies.

We appreciate your time in reading our Lululemon Athletica Deep Dive. We will continue tracking LULU’s performance and strategic evolution through periodic updates and implication reports available to subscribers.

Disclaimer

This report is for informational and educational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. All opinions expressed reflect the author’s judgment as of the publication date and are subject to change without notice.

The author does not currently hold shares of Lululemon Athletica (LULU) but may initiate a position in the future without further notice.

For the full disclaimer, click here.

Copyright © 2025 Business Deep Dives. All rights reserved.

Business Deep Dives is an independent research publication operating on a pre-incorporation basis. All content is protected under applicable international copyright principles.

LULU’s resilience feels less a bit about athleisure demand itself and instead, more about the resilience of the brand

When consumers get price-sensitive, they don’t evenly trade down, they will consolidate spend instead.

True premium brands will bleed slower while middle tier bleed out.

Good article, great insights and research